Advice to Novice Investors

Five Steps to Wise Investing

- Step One: Choose a Brokerage

- Step Two: Open an IRA

- Step Three: Assess Your Risk Aversion

- Step Four: Diversify Diversify Diversify

- Step Five: Stay Informed

- Other Thoughts

1. Choose a Brokerage

Should you go with the straightforward, cost-effective service, or opt for the pricier, more service-oriented experience?

Before deciding which type of brokerage account to open, it’s wise to get a better understanding of your options. This will include comparing the services and features offered, minimum opening balance requirements, research and investment tools provided, and the cost of commissions and fees.

Traditional full-service brokerages

With brokerage accounts, you can buy and sell stocks, bonds, mutual funds, exchange-traded funds and other investment products.

Traditional “full-service” brokers do more than just facilitate the buying and selling of a stock or bond. These brokers tend to offer a wide array of services and products, including financial and retirement planning, investing and tax advice and regular portfolio updates.

Since you are getting personalized recommendations and service, traditional brokerages often come with higher fees, generally charging 1-2% on the assets managed. For instance, a $100,000 portfolio would cost $1,000 to $2,000 in fees annually. That could dig into your profits over the long run.

Traditional brokerage fees are something to carefully consider, especially if you are investing and planning for your retirement. But if you really don’t want to invest on your own—instead preferring personalized advice and guidance—then a traditional brokerage could be the right choice.

Discount brokerages

A discount or reduced service brokerage could be a better choice for the fee-conscious investor who prefers to go it alone. These brokerages will generally not offer investment advice, although it’s common for a discount brokerage to offer free research and educational tools to help you make better investing decisions.

Discount brokers come in all shapes and sizes. Some will provide better investing tools than others, but charge higher fees, while others might provide only the basics, but charge the lowest fees. Examples of popular discount brokerages include E-Trade, Sharebuilder, Scottrade and TD Ameritrade.

With a discount brokerage, you can either execute a trade online automatically through a computerized trading system, or call in your order with a broker over the phone—although the latter option will likely cost you more. Some discount brokers charge annual account fees, although this often isn’t the case. However, you’ll likely just have to pay a $5 to $10 commission fee on each buy or sell order, although the actual cost will depend on your broker.

Another thing to consider is each broker’s minimum opening balance requirement. Some brokers could require as low as zero to $500 to open an account, while others could require $1,000 or more. Some brokers might charge you a fee if your balance falls below a certain amount. These are just a few things to keep in mind when selecting your broker.

When it comes to investing for retirement, discount brokers could be an easier, lower-cost option. If you do prefer one-on-one guidance, keep in mind that some discount brokerages offer personalized investment recommendations or professionally managed portfolios at an additional cost.

- Reduced Service Online Brokerages

- Full Service Online Brokerages

-

Roth vs. traditional IRA? How to choose

Consider the tax benefits of each. Consider a traditional IRA to get a tax break now, and a Roth IRA to reduce your taxes in the future.

Calculate your Roth IRA contribution amount. Find out how much you’re eligible to contribute.

Calculate your traditional IRA contribution amount. Find out how much you can deduct.

Compare early withdrawal fees and penalties. The IRS has different rules for borrowing money or withdrawing cash from a Roth versus a traditional IRA before age 59½.

Consider benefits after retirement. Factor in how long you want your money to remain invested and how much you want to leave to your heirs.

- Tax benefits of Roth and traditional IRAs

- How willing are you to take a risk, that is, to pursue and uncertain positive outcome with the potential that a negative outcome could result instead?

- What is your risk capacity: your financial ability, in dollars, to endure potential financial loss and still be able to achieve your goals?

- How risky do you perceive a market or an investment? Everyone's perception of risk is unique (which makes studying markets so interesting and so frustrating).

- Rutgers University

- Charles Schwab

- Wells Fargo

- Bankrate

- Most volatile in the short term

- Represent shares of ownership in publicly held companies

- Historically have outperformed other investments over long periods (keep in mind that past performance does not guarantee future results)

- Returns and principal will fluctuate so that accumulations, when redeemed, may be worth more or less than original cost

- More stability than stocks

- Set rate of interest

- Value fluctuates due to current interest and inflation rates

- Includes "guaranteed" or "risk-free" assets

- Also includes money market instruments (short-term fixed income investments)

- Helps protect future purchasing power as property values and rental income run parallel to inflation

- Values tend to rise and fall more slowly than stock and bond prices. It is important to keep in mind that the real estate sector is subject to various risks, including fluctuation in underlying property values, expenses and income, and potential environmental liabilities.

- Values tend to exhibit low correlations with stock and bond prices.

- Price dynamics are also unique: commodities become more volatile as prices rise. Thus a commodity with a 20% volatility might have a 50% volatility if prices doubled.

- Helps protect future purchasing power as values have fixed utility and thus run parallel to inflation

- Tolerance for risk (market volatility)

- Goals and investment objectives

- Preferences for certain types of investments within asset classes

- Investopedia Best for: Looking up the definition of a QTIP Trust and figuring out if you need one.

- Kiplinger Best for: Keeping on top of the latest investing news.

- LearnVest Best for: Reading what certified financial planners think about budgeting, spending, saving, and more.

- NerdWallet Best for: Finding the highest-yield savings account to store your money.

- Quora Best for: Readers who already have a basic understanding of financial concepts.

- CNN Money Best for: Learning how the news affects your money.

- New York Times: Your Money Section Best for: Following the ins and outs of new financial regulations, rules, and changes.

- Rockstar Finance Best for: Reading essays and reflections from personal finance bloggers across the web.

- Wise Bread Best for: Advice on the everyday challenges of spending less and saving more.

- Credit.com Best for: Figuring out why your credit score keeps dropping.

- Jim Blankenship, Financial Ducks In A Row; @FinancialDucksinaRow

- Josh Brown, The Reformed Broker; @reformedbroker

- Ben Carlson, A Wealth of Common Sense; @awealthofcs

- Kathryn Cicoletti, Ms. Cheat Sheet; @mscheatsheet

- Sam Dogen, Financial Samurai; @financialsamura

- Jim Dahle, The White Coat Investor; @WCInvestor

- John Roberson, Evil Finance Guy

- Robinhood (iOS, Android) no-fee trades.

- Betterment (web, iOS, Android) uses sophisticated algorithms to find the best and cheapest fund mix

- Wealthfront (web, iOS, Android) 20 portfolios that they manage and you can invest in

- Openfolio (web, iOS) compare your portfolio's performance with that of 70,000 other investors

- FeeX (web) learn just how much you're paying in fees

- Estimize (web) crowdsources earnings estimates from over 24,000 people

- StockTwits (web, iOS, Android) 1.4 million users chat about stocks, bonds, currencies, futures, oil, gold, etc.

Back to Top

2. Open an Individual Retirement Account (IRA)

The biggest difference between a Roth and a traditional IRA is how and when you get a tax break. If you're early in your career and anticipate that your income will increase significantly over time a Roth IRA makes sense.

Traditional IRA: The benefit of a traditional IRA is that your contribution is tax deductible. Taxes come due in retirement when you take distributions, or make withdrawals, from the IRA.

Roth IRA: The benefit of a Roth IRA is that your withdrawals in retirement are not taxed. A Roth IRA operates in reverse of a traditional IRA: You pay taxes upfront, meaning your contributions are not deductible.

One thing that Roth and traditional IRAs have in common is that in both accounts, earnings on your investments grow tax-free.

Consider Your Current and Projected Tax Bracket

To help you figure out which tax setup will be most beneficial to you in the future, let’s start with your present: What’s your current tax bracket?

If you’re currently in a low tax bracket (anything in the low 20% range or lower), a Roth IRA is probably a good choice. This is more likely the case if you’re in the early stages of your career, or you’ve changed careers and will be at a higher rung of the income ladder when you retire.

Why a Roth? Withdrawals from a Roth IRA in retirement are not subject to income tax. So when your future flush self starts drawing income from your Roth IRA savings, you won’t have to pony up income taxes to the IRS when your tax rate has gone up.

I created this chart to show the time value of an investment of $1,000 over 40 years at 5% growth in both a

Roth IRA

in green and a Traditional IRA

in red. The Roth investment is reduced by income tax on the front end and growth is tax-free, whereas all funds in the traditional IRA—original investment plus all growth—are taxed at the time of withdrawal.

If you’re in a high tax bracket or close to retirement age, a traditional IRA makes more sense. Why? A traditional IRA enables you to take a tax deduction later when your fixed retirement income will be lower than your income is now. This is the reasoning behind tax shelters.

In other words, after their 40s or 50s people tend to migrate to a lower tax bracket due to full- or semi-retirement, taking on lower-paying but more meaningful work, or simply needing to draw less income if expenses have gone down. And since withdrawals from a traditional IRA are taxable as income as long as they’re taken after age 59½, by choosing a traditional IRA you save again on the backside because you’re taking out that money when you’re in a lower tax bracket.

Regardless of your choice of an investment vehicle here's a brief video with good advice for those starting out on their path to retirement.

Back to Top

3. Assess Your Risk Aversion

Investor, know thyself...

Risk is a hard-to-define aspect unique to human behavior. In prescribing your optimal behavior as an investor, the question is three-fold:

Here's one financial advisor's illustration of the variables involved in assessing your risk aversion:

There are many online quizes to help you assess your ability to manage risk, all of them helpful, none all inclusive. Here are a few:

There's usually a correlation between risk and reward: the greater the risk, the greater the reward.

Back to Top

4. Diversify Diversify Diversify

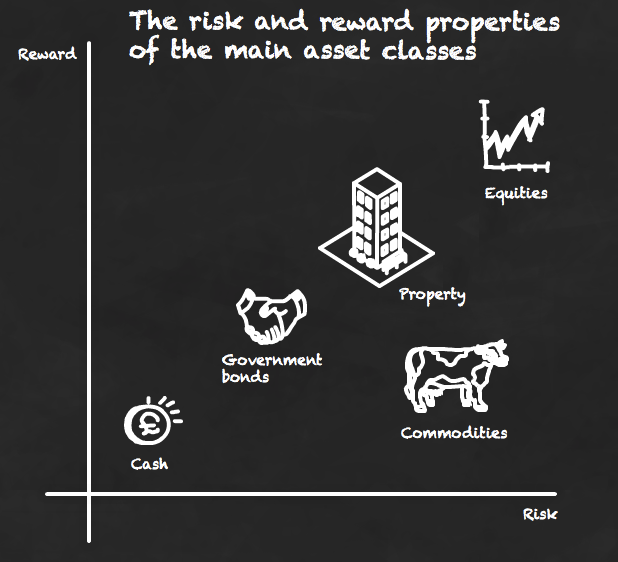

An asset class is a group of instruments which have similar financial characteristics and behave similarly in the marketplace. We can often break these instruments into those having to do with real assets and those having to do with financial assets. Often, assets within the same asset class are subject to the same laws and regulations; however, this is not always true. For instance, futures on an asset are often considered part of the same asset class as the underlying instrument but are subject to different regulations than the underlying instrument.

Many investment funds are composed of the two main asset classes which are securities: equities (stocks) and fixed-income (bonds). However, some also hold cash and foreign currencies. Funds may also hold money market instruments and they may even refer to these as cash equivalents; however, that ignores the possibility of default. Money market instruments, being short-term fixed income investments, should therefore be grouped with fixed income.

In addition to stocks and bonds, we can add cash, foreign currencies, real estate, and commodities to the list of commonly held asset classes. In general, an asset class is expected to exhibit different risk and return investment characteristics, and to perform differently in certain market environments.

Asset classes and asset class categories are often mixed together. In other words, describing large-cap stocks or short-term bonds asset classes is incorrect. These investment vehicles are asset class categories, and are used for diversification purposes. They're not listed in any order of volatility/riskiness.

Stocks - Also called equities

Fixed income - Fixed income, or bond investments, generally pay a set rate of interest over a given period, then return the investor’s principal.

Cash

Foreign Currencies

Real estate - Your home or investment property, plus shares of funds that invest in commercial real estate.

Commodities - Physical goods such as gold, copper, crude oil, natural gas, wheat, corn, and even electricity.

Most financial experts agree that some of the most effective investment strategies involve diversifying investments across broad asset classes like stocks and bonds, rather than focusing on specific securities that may or may not turn out to be "winners." Diversification is a technique to help reduce risk. However, there is no guarantee that diversification will protect against a loss of income.

The goal of asset allocation is to create a balanced mix of assets that have the potential to improve returns, while meeting your:

Being diversified across asset classes may help reduce volatility. If you include several asset classes in your long-term portfolio, the upswing of one asset class may help offset the downward movement of another as conditions change. But keep in mind that there are inherent risks associated with investing in securities, and diversification doesn’t protect against loss.

Back to Top

5. Stay Informed

There's an abundance of good advice on the Internet. Your challenge: find the best of it. Because if you don't you're not a serious investor. It's like being in an endless college course where there's never a 'final' but there's a quiz every day. You're competing in an immense class of very smart people.

Money Management and Investment Advice sites:

Blogs:

Apps:

Back to Top

Other Thoughts

Investing in the stock market takes discipline in order to be successful. Jumping in blind with no more idea of what to do other than “buy low, sell high” is the quickest way to lose your money. Without some guidelines to help you out along the way, it’s easy to make mistakes and get discouraged.

The good news is that investing isn’t rocket science. Even the smartest Ivy League college graduate knows that successful investing means following the rules. So before you start navigating the traffic on Wall Street, here are simple rules that will enrich your investing experience:

Know What You Own – The hottest new tech company may be all Wall Street and your friends are talking about but if you don’t understand what it is the company does or how they actually make a profit, take a pass on it.

Stay Calm And Keep Investing – Panicking when the market is behaving erratically is the quickest way to big losses. Don’t get sucked up in the hype and remember when everyone is selling, you should be buying and vice versa.

Don’t Fall In Love – Remember that stocks are just investments. You may really like a certain company, but if a better opportunity comes along you can’t be afraid to chase it down.

Filter Out The Noise – Wall Street always has a new crisis or a new big opportunity for you to worry about. Ignore the pundits and stay focused on the fundamentals. (Some noise sources: Yahoo, Bloomberg, MarketWatch.

Explain Why You Own A Stock – Know why you want to own a particular stock. Is there a reason you think it’s going to appreciate? Before buying, be able to explain to a stranger why you think the stock is worth owning.

Make a Habit of Practicing Due Diligence – It might not be fun, but sticking to your due diligence will keep you from making costly mistakes. If the fundamentals of the company are sound, the technicals will take care of themselves in the long run.

Don’t Be Afraid To Cut Your Losses – It’s never fun to admit defeat and even less fun to sell a stock at a loss. But if you own a loser, you need to cut it loose before it does more damage to your portfolio.

Cash Is Also An Asset Class – Too many investors think that they need to be all-in in order to be a successful trader. Keeping cash on the sidelines, though, means that when an opportunity presents itself you can act quickly without having to sell out of another investment before you’re ready.

Pigs Get Fat, Hogs Get Slaughtered – Once a stock you own has made the profits you expected, it’s time to move on. Don’t hold on and try to squeeze every last drop of profits from a stock or you could end up losing all the gains you made on paper.

And Finally...

As you become more experienced with trading, you may decide on a few rules of your own to help you stay focused. Always keep an eye on your bottom line.

Back to Top